Macro Snapshot: The week ending June 5 belonged to two central banks and one labour number. On Friday June 5, the Reserve Bank of India’s Monetary Policy Committee held the repo rate at 5.25% for the third consecutive meeting, voting unanimously, and raised the FY27 inflation projection by 50 basis points to 5.1%. Hours later, the US Bureau of Labor Statistics released a May nonfarm payrolls print of 172,000 jobs, roughly double the consensus expectation of approximately 85,000. The number was the third consecutive beat, and it triggered an immediate repricing across rates, currencies, and metals. The US 10-year Treasury yield rose around 6 basis points to close at 4.55%, the 30-year crossed 5.0%, and CME FedWatch probabilities shifted to near-fully pricing a Fed rate hike by year-end. Fed Chair Kevin Warsh, who took office in late May, enters his first FOMC meeting on June 16-17 with a labour market that complicates any dovish framing.

The rupee weakened steadily through the first four days of the week, losing approximately 1% against the dollar as oil remained elevated and institutional outflows continued. On Friday, the rupee reversed and firmed after the RBI announcement and a broader equity selloff that weakened the dollar. RBI Governor Sanjay Malhotra clarified that the central bank does not target any specific level or band for the rupee. The government concurrently announced a tax relief package for foreign investors in government securities, removing long-term capital gains tax and potentially reducing the 20% withholding tax on interest income, a structural attempt to support the rupee through the FAR route without forcing the RBI into rate action. On the geopolitical side, Iran’s Foreign Minister Abbas Araghchi stated no meaningful progress had been made in ceasefire negotiations, and Iran-backed Hezbollah rejected a US-mediated ceasefire proposal, keeping the risk premium intact and Brent crude on its weekly gain.

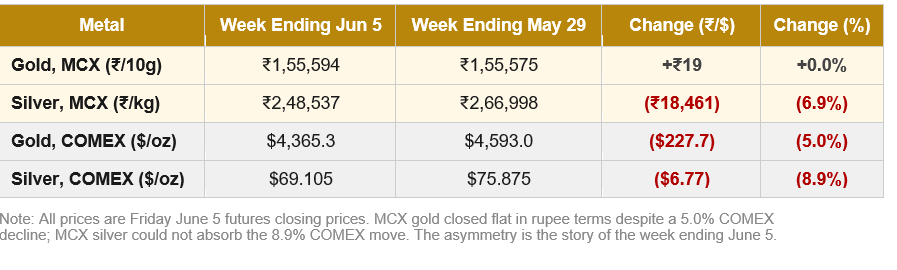

Gold-specific drivers. The World Gold Council’s Central Bank Gold Statistics report for June 2026 confirmed that central banks globally returned to net buying in April, purchasing 17 tonnes after net sales in March. Poland led with 14 tonnes, taking year-to-date purchases to 45 tonnes. China added 8 tonnes, its highest monthly purchase since December 2024, extending a streak of 18 consecutive months. Reserves now stand at approximately 2,322 tonnes. The Czech National Bank added 3 tonnes, its 38th consecutive monthly purchase. Russia continued its sales streak (6 tonnes in April, 22 tonnes year-to-date). On the domestic side, the May 13 import duty hike from 6% to 15% (total levy now 18.45% with IGST) continues to define the Indian gold market. The WGC’s earlier India update flagged a record domestic discount of $145-150 per ounce to the landed price, and that gap is what allowed MCX gold to absorb the 5.0% COMEX decline almost entirely in the week ending June 5. The cushion remains in place, but it cannot expand indefinitely.

Silver-specific drivers. The Silver Institute’s World Silver Survey 2026 projects a sixth consecutive annual supply deficit of 46.3 million ounces, widening from 40.3 Moz in 2025. Cumulative drawdown from above-ground stocks since 2021 stands at approximately 762 million ounces. The structural composition has shifted across 2025 and 2026: solar PV silver demand is expected to decline approximately 19% in 2026 to around 151 million ounces as manufacturers aggressively thrift and substitute at current price levels. The offset comes from retail investment: coin and bar demand rose 14% in 2025, with India up 33%. Silver runs on two demand engines, industrial and monetary, and the May NFP shock hit the monetary engine directly. COMEX silver fell 8.9% in the week ending June 5 versus gold’s 5.0%; the gold-silver ratio widened as a result. The deficit story remains structurally intact, but rate data moves prices on a weekly horizon while it does not move ounces.

Gold | MCX GOLD1!

The most recent candle is a bearish expansion bar: price opened near the session highs around 1,58,500, rejected the 1,58,500 to 1,60,000 zone, and closed near 1,55,500. Sellers were active on recovery attempts rather than allowing price to accept higher. The bounce into 1,59,000 to 1,60,000 has failed, and that zone is now short-term supply.

Immediate demand sits in the 1,54,500 to 1,55,500 zone. Price has tested into that area, but the close is not clearly below it. This is pressure into demand, not a confirmed breakdown. The old declining trendline from the late-January high is no longer the active battleground; price has been trading well above it for several weeks. The more relevant signal is the failure to build higher acceptance after the mid-May spike and the developing pattern of lower highs below 1,60,000. The upside continuation structure is weakening, and confirmation of a structural break needs a close below 1,54,500 to 1,55,000.

With COMEX gold falling 5.0%, the duty-discount mechanic absorbed almost the entire dollar move in rupee terms. MCX gold gained ₹19 per 10g. The same cushion that produced the record $145-150 per ounce domestic discount continues to insulate domestic pricing, but it is doing so against a backdrop of weakening technical structure. The two questions that matter most: whether the 1,54,500 to 1,55,500 demand zone holds, and whether the demand cushion can keep absorbing further COMEX weakness.

| Key Takeaway: Gold is in an attempted breakdown into the ₹1,54,500 to ₹1,55,500 demand zone after failing to reclaim ₹1,59,000 to ₹1,60,000 supply. The short-term bias is bearish, but confirmation requires a close below demand. The larger uptrend from the February lows remains intact unless that demand breaks. For Indian traders and jewellers, the rupee-and-duty cushion has done the heavy lifting in the week ending June 5; MCX gold has not had to follow COMEX’s 5.0% decline. The risk in extrapolating that comfort is that the cushion has limits. Inventory holders benefit from current MCX stability; replacement-cost watchers should pay closer attention to the international tape than the domestic chart suggests. |

Silver | MCX SILVER1!

Silver’s most recent candle is a decisive bearish expansion bar. Price rejected near 2,60,000 to 2,62,000, broke sharply lower, and closed near 2,48,500. This is impulsive selling, not a slow drift. The 2,70,000 to 2,78,000 recovery shelf failed to attract follow-through, and the pattern of lower highs that developed in late May resolved into a lower-low break in the June 5 session.

The 2,60,000 to 2,65,000 demand zone, which had been the structural support line flagged in earlier weekly notes as the line between healthy pullback and confirmed breakdown, has now been broken. Until reclaimed, it should be treated as near-term supply. Price is reacting into the older 2,47,000 to 2,50,000 base. A bounce from there is possible, but unless price quickly reclaims 2,60,000 to 2,65,000, that bounce will be a reaction within a confirmed downtrend rather than a structural reversal.

The upside breakout structure that defined the April and May advance is invalidated in the short term. Silver has produced a clean lower-low break, and the bearish structural shift is confirmed on the daily chart. COMEX silver fell 8.9% in the week ending June 5, nearly twice gold’s decline, and the gold-silver ratio widened toward 63. The duty-and-rupee cushion absorbed only about 2 percentage points of relative outperformance versus the COMEX move. With the international tape impulsive and the domestic technical structure broken, silver is in a more difficult position than at any point since the early April recovery.

| Key Takeaway: Silver has a confirmed breakdown below ₹2,60,000 to ₹2,65,000 after a failed recovery above ₹2,70,000 to ₹2,78,000. Momentum is bearish unless price rapidly reclaims the broken demand zone. The next support is the ₹2,47,000 to ₹2,50,000 base. Position sizing matters more here than in gold given silver’s impulsive character on both the upside and downside. The structural deficit narrative from the World Silver Survey 2026 remains intact, but it is a multi-year thesis being tested by a multi-week rate-hike repricing. Tactical patience makes more sense than tactical aggression. |

Special Focus | Central Banks Return to Net Buying:

The World Gold Council’s Central Bank Gold Statistics report, published in early June, deserves attention separately from the macro and technical sections because it tells a different story from the price action.

Net buying resumed in April. After net sales in March, global central banks bought 17 tonnes net. Poland led with 14 tonnes, taking its year-to-date total to 45 tonnes and reserves to approximately 595 tonnes (30% of total). China added 8 tonnes, extending its buying run to 18 consecutive months and taking official reserves to approximately 2,322 tonnes (9% of total). The Czech National Bank added 3 tonnes, its 38th consecutive monthly purchase. Russia continued its sales streak (6 tonnes in April, 22 tonnes year-to-date). Turkey reported virtually flat reserves with short-term gold/USD swaps maturing.

The consistency story is the structural story. Year-to-date, Polish (45t), Uzbek (24t), Chinese, Kazakh, and Czech buying has been the visible engine. Over a trailing 36-month window, Eastern European and Asian central banks have purchased 12 tonnes and 11 tonnes per month on average respectively, with global central bank average net purchases of 29 tonnes per month over the same period. This is a durable, multi-region bid that has continued through every cycle of rate expectations and every geopolitical episode.

The forward signal. The WGC’s Central Bank Gold Reserves Survey 2026 is due for release in June. The 2025 survey showed 95% of respondent central banks expected global gold reserves to increase over the following 12 months (up from 81% in 2024), and 43% expected their own reserves to increase (versus 29% in 2024). The central bank bid is the slow-moving institutional foundation under the cyclical price story. When rate-cycle noise dominates short-term price action (as it did in the week ending June 5), the structural bid does not disappear; it becomes less visible.

Source: World Gold Council, Central Bank Gold Statistics, June 2026. Used in line with fair industry practice with citation to the World Gold Council as source.

Watch in the Days Ahead:

- FOMC June 16-17 (Kevin Warsh’s first meeting): Markets are pricing a hold with roughly 97% probability. The language around the path forward is what matters. Any tilt toward acknowledging hike optionality will extend pressure on both metals. A dovish surprise from a Warsh-led committee would be a significant positive catalyst.

- US CPI release (June 11): Core PCE remains at 3.3%. A higher-than-expected print would reinforce rate-hike pricing. A soft print would partially restore the rate-cut thesis and ease pressure on precious metals.

- Iran developments and oil: The conflict entered its fourth month with no resolution in sight. Any credible de-escalation signal would reduce the geopolitical risk premium embedded in gold. A further escalation, particularly involving the Strait of Hormuz, would produce the opposite. Both scenarios are live.

- RBI inflation forecast follow-through: The 50 basis point upward revision in the FY27 inflation projection to 5.1% shifts the implied rate path further out. At least one analyst now sees the first RBI rate hike materialising by February 2027 if oil and rupee pressures persist. Upcoming domestic CPI prints will confirm or challenge the higher inflation trajectory.

- MCX key technical levels: Gold: ₹1,54,500 to ₹1,55,500 demand must hold to keep the larger uptrend intact; ₹1,59,000 to ₹1,60,000 supply must clear for the breakout to resume. Silver: ₹2,60,000 to ₹2,65,000 must be reclaimed to repair the broken structure; failing that, ₹2,47,000 to ₹2,50,000 is the next support, and a break below opens the path toward ₹2,30,000 to ₹2,40,000.

- FII flow response to G-Sec tax relief: If foreign inflows pick up materially, the rupee gets a tailwind, which would reduce the MCX premium that cushioned domestic gold in the week ending June 5. Flow data in the days ahead will indicate whether the policy is having the intended effect.

Disclaimer: This article is for informational purposes only and does not constitute investment or trading advice. All prices are futures closing prices, MCX in INR, COMEX in USD. The Special Focus section draws on data from the World Gold Council Central Bank Gold Statistics report (June 2026), used in line with fair industry practice with citation to the World Gold Council as source. Past performance is not indicative of future results.

Authored by Dhawal Chotai