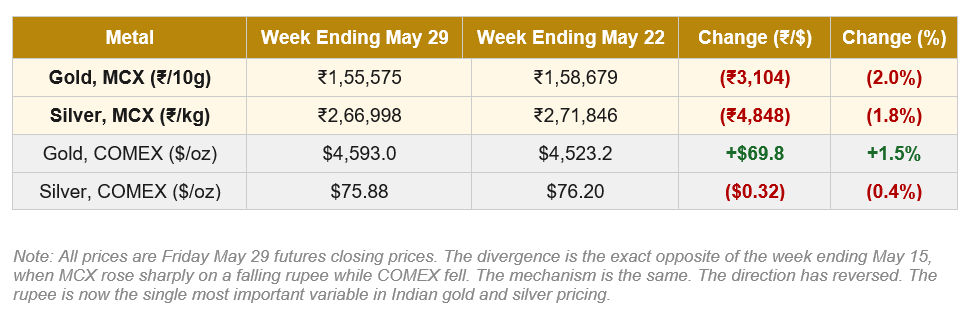

Macro Snapshot: Two weeks ago, the rupee crisis pushed MCX gold up 3.9% while COMEX gold fell 3.6%. The week ending May 29 produced the exact mirror image: COMEX gold rose 1.5% while MCX gold fell 2.0%. Same mechanism, opposite direction. The rupee’s path through the week tells the full story. The intra-week range of 95.05 to 96.26, roughly 1.2%, is what explains why MCX prices fell while COMEX prices rose. But US and Iranian negotiators reached a tentative agreement on Thursday to extend the three-month-old ceasefire by 60 days, with talks beginning on Iran’s nuclear program and, critically, unrestricted commercial shipping through the Strait of Hormuz causing Brent crude to fall to $92.66/barrel. Indian precious metals pricing is now a two-variable problem: international price direction plus rupee direction. Track only one and you will be wrong half the time.

India’s structural backdrop also continues to weaken. Forex reserves fell to a 14-month low of $681.4 billion, down $37 billion from their peak, and FII outflows have crossed $24 billion since the start of 2026. Fuel prices were raised for the first time in four years, confirming the energy shock is feeding directly into household inflation. The RBI June 6 MPC meeting is one week away, with markets pricing a possible rate hike. Any rate action will be felt immediately through the rupee channel into MCX prices.

Gold drivers: COMEX gold hit a two-month low of $4,380 on Wednesday before rebounding sharply on the ceasefire extension and in-line PCE data. The recovery was real but fragile: Trump has not approved the proposed terms, Vance has cautioned against premature optimism, and Iran’s Supreme Leader recently directed that enriched uranium should not leave the country. On the domestic side, the large MCX discount to the official landed price (flagged by the WGC as historically unprecedented) will narrow as the inauspicious buying season ends and pre-Diwali planning begins. That narrowing is a structural upside force for MCX gold regardless of international price direction.

Silver drivers: Silver sits at an intersection of two forces that partially offset. Structurally, it is in its fifth consecutive year of supply deficit, driven by record solar PV demand (projected at 230 million ounces in 2026 per the Silver Institute), electronics and 5G consumption (approximately 240 million ounces annually, 8 to 12% growth), and AI data centre infrastructure. Over 70% of global silver production is a by-product of copper and zinc mining, which means supply cannot respond quickly to higher prices. The Hormuz closure has also suppressed silver’s industrial demand base by disrupting the broader base metals supply chain. A genuine reopening would therefore benefit silver on two channels: lower oil reducing inflation pressure, and restored fabrication demand. In the short term, the ceasefire-driven rupee appreciation pushes MCX silver lower. In the medium term, silver’s industrial recovery story remains structurally intact.

Gold | MCX GOLD1!

Gold has deteriorated meaningfully from the prior week. The tight post-breakout shelf around ₹1,58,000 to ₹1,60,000 that held through the week ending May 22 has now broken. Price slipped out of that shelf and closed lower at ₹1,55,575. The rejection from ₹1,62,000 to ₹1,64,000 has started to matter more. What initially looked like a normal pause after breakout is now becoming a controlled downside drift, with recent candles showing lower highs and weaker closes.

Price is now testing the ₹1,54,000 to ₹1,56,000 breakout-retest zone, the same zone that previously acted as the upper end of the old consolidation range. The quality of the reaction here determines the next move. The declining trendline breakout from the week ending May 15 is not invalidated yet, but it is weakening. Gold is no longer comfortably above the breakout area. It is now sitting on the edge of it. The latest candle shows some intraday demand near the retest zone, but the close remains weak, suggesting a reaction from demand rather than a confirmed reversal.

| Key Takeaway: Gold has moved from post-breakout consolidation into an attempted retest of ₹1,54,000 to ₹1,56,000 breakout support. The breakout is technically alive but under pressure. Acceptance below ₹1,54,000 would turn this into a failed breakout and early breakdown. Tranche-based accumulation remains the appropriate strategy until the breakout zone either holds convincingly or breaks. |

Silver | MCX SILVER1!

Silver has also weakened, but the nature of the move is different from gold. The prior week was mainly a consolidation after the failed spike near ₹2,95,000 to ₹3,00,000. The week ending May 29 saw that consolidation start resolving lower. Price has slipped from the earlier ₹2,70,000 to ₹2,76,000 holding range and is now pressing into the ₹2,60,000 to ₹2,65,000 demand and breakout-retest zone. The failed breakout near ₹3,00,000 remains the dominant short-term event. The market has not been able to reclaim that lost momentum, and recent candles show lower highs after the exhaustion move.

However, the latest weakness has not yet become a confirmed breakdown. The wick into the ₹2,60,000 to ₹2,65,000 zone shows that buyers are still reacting from demand rather than allowing clean acceptance below it. The broader breakout structure remains valid only because price is still above the main demand base. But the immediate structure has clearly shifted from bullish expansion to corrective distribution. A close below ₹2,60,000 to ₹2,65,000 would turn this into an early breakdown. A move back above ₹2,80,000 would be needed to repair short-term momentum.

| Key Takeaway: Silver has moved from corrective consolidation into an attempted retest of ₹2,60,000 to ₹2,65,000 demand. The ₹2,95,000 to ₹3,00,000 breakout has already failed, but the broader breakout has not fully failed unless price accepts below ₹2,60,000 to ₹2,65,000. The move has shifted from bullish expansion to corrective distribution. A hold at the demand zone keeps the recovery structure intact. A break opens the path to ₹2,40,000 to ₹2,45,000. Upside repair requires a close above ₹2,80,000. Silver remains the stronger medium-term chart between the two metals, but gold is currently less technically damaged short-term. |

Watch in the Days Ahead:

- RBI MPC (June 6): The most important event for Indian gold and silver in the near term. A rate hike would be sharply rupee-positive and therefore bearish for MCX prices. A hold despite continued rupee stress would signal growth prioritisation over currency defence, which would be rupee-negative and MCX-supportive. The statement’s language on the rupee, imported inflation, and gold import policy will all be scrutinised by trade participants and bullion dealers.

- Iran ceasefire durability: The 60-day extension is tentative. Trump has not approved the terms. Vance has cautioned against premature optimism. Iran’s Supreme Leader recently directed that enriched uranium should not leave the country, complicating the nuclear negotiation track. If the ceasefire holds and Hormuz reopens for commercial shipping, oil falls, the rupee strengthens, and MCX prices face further downside pressure from the currency channel. If the ceasefire collapses, the opposite. For silver specifically, a genuine Hormuz reopening would also restore three months of suppressed industrial demand, adding a bullish force that gold does not have.

- Silver supply deficit and solar demand: Silver’s fifth consecutive year of structural supply deficit is being driven by record solar PV demand (projected at 230 million ounces in 2026), electronics consumption (240 million ounces annually with 8 to 12% growth), and AI data centre infrastructure. Over 70% of silver production is by-product, limiting supply response. This structural backdrop is the reason the medium-term bull case for silver remains intact even through the current technical correction. Watch for any data on global solar installation rates and semiconductor order books for signals on whether industrial demand is accelerating or moderating.

- Forex reserves and import policy: Reserves at $681.4 billion are at a 14-month low with $37 billion drawn down from peak. The rate of drawdown is unsustainable if the current account deficit continues widening. Watch weekly reserve data closely. A further sharp decline would increase the probability of additional gold and silver import restrictions, which would move MCX prices and alter the trade landscape further.

- MCX key levels: Gold: ₹1,54,000 to ₹1,56,000 breakout support being tested now. Acceptance below ₹1,54,000 turns the breakout into a failure. ₹1,48,000 to ₹1,50,000 is the next major demand zone. Silver: ₹2,60,000 to ₹2,65,000 is the structural demand. A break below opens the path to ₹2,40,000 to ₹2,45,000. Upside repair requires a close above ₹2,80,000.

Disclaimer: This article is for informational purposes only and does not constitute investment or trading advice. All prices are futures closing prices, MCX in INR, COMEX in USD. Past performance is not indicative of future results.

Authored by Dhawal Chotai