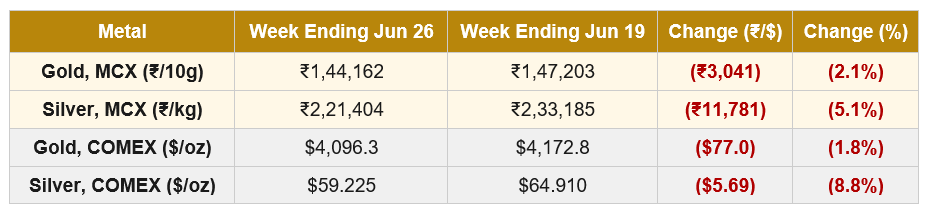

Macro Snapshot: The week ending June 26 extended the precious metals selloff to a fifth consecutive week and pushed both gold and silver into the most important long-term technical zone of the broader uptrend: the 200-day exponential moving average. Three macro forces drove the decline, and they did so simultaneously.

First, the US-Iran 60-day peace roadmap, formally signed in Switzerland on June 17, continued to remove the geopolitical risk premium that had supported the metals since the February conflict began. Crude oil collapsed as a result: WTI settled below $70 per barrel for the first time since February 28, closing at $69.23 on Friday, while Brent fell to $71.99. Oil has effectively returned to pre-conflict levels. The decline was complicated late in the week when the Islamic Revolutionary Guard Corps struck the Singapore-flagged cargo vessel Ever Lovely in the Strait of Hormuz on Thursday June 25, prompting the International Maritime Organization to pause the evacuation of approximately 11,000 stranded sailors. Oil rose briefly on the news before resuming its decline as broader supply concerns eased.

Second, the May Personal Consumption Expenditures data, the Fed’s preferred inflation gauge, was released on Thursday June 25. Headline PCE accelerated to 4.1% year-on-year, the highest since April 2023 and the fourth consecutive monthly acceleration, matching consensus. Core PCE rose to 3.4% year-on-year, a slight beat versus the 3.3% forecast and the highest since October 2023. On a monthly basis, headline PCE rose 0.4%, below the 0.5% forecast. The data did not surprise the market in either direction, but it confirmed the picture that the Fed and Chair Kevin Warsh laid out at the June 17 FOMC: inflation remains stubbornly above the 2% target, and rate hikes are now on the table for 2026 rather than rate cuts. CME FedWatch shows approximately 80% odds of a December hike and 62-63% odds of a September move. The dot plot from the June FOMC implies a median of at least one hike before year-end, with several committee members projecting two.

Third, the rates-and-dollar mechanism continues to weigh on the metals as an ongoing structural factor. The framework is straightforward: when US interest rates rise (or are expected to rise), the dollar strengthens; when the dollar strengthens, gold and silver, which are priced in dollars, become more expensive for non-US buyers and lose purchasing-power appeal globally. In the week ending June 26, the US Dollar Index briefly hit a 13-month high mid-week before easing on the PCE print. The US 10-year Treasury yield actually fell roughly 7 basis points on the week to close at 4.376%, but inflation expectations fell faster than nominal yields (because oil collapsed), keeping real yields elevated. Real yields, not nominal yields, are what matter for gold; gold fell despite the headline yield decline because the underlying real-yield headwind remained intact. The rupee was range-bound between 94.2 and 94.9 through the week and closed roughly flat against the dollar, providing neither a cushion nor an amplifier to the international move.

Gold-specific drivers: Gold spot dropped below $4,000 per ounce on Wednesday for the first time since November 2025 before recovering to close near $4,096. The price action in the week ending June 26 effectively unwound the geopolitical premium that had been built up since late February: oil prices have now returned to pre-conflict levels (around $70 WTI versus the average $103 during March), and gold has now retraced more than 25% from its January 28 all-time high of $5,589. The structural bid remains central banks bought 244 tonnes in Q1 2026, the World Gold Council’s June survey showed a record 45% of central banks plan to add gold over the next 12 months, and the ECB has confirmed that gold has overtaken US Treasuries as the world’s top reserve asset. The structural bid and the cyclical price action continue to run on different clocks. MCX gold’s 2.1% decline closely tracked COMEX’s 1.8% move because the rupee was effectively neutral.

Silver-specific drivers: Silver fell 8.8% on COMEX, more than four times gold’s decline, and the gold-silver ratio widened to approximately 70:1 at one point during the week. This is up sharply from the 55:1 level in early May and the 50:1 reading at silver’s January all-time high. The ratio reflects silver’s dual exposure: the monetary engine is being hit by rate-hike repricing and dollar strength, while the industrial engine faces headwinds from lower energy prices (which signal slower global growth) and dollar strength (which makes silver more expensive for non-US buyers). The Silver Institute’s structural deficit thesis (46.3 Moz projected for 2026) remains intact, but cyclical price action is being driven by macro positioning, not physical supply-demand. MCX silver fell 5.1% versus COMEX’s 8.8%, suggesting the rupee dynamic provided a partial cushion in the week ending June 26, in contrast to the two prior weeks where it had added to the decline.

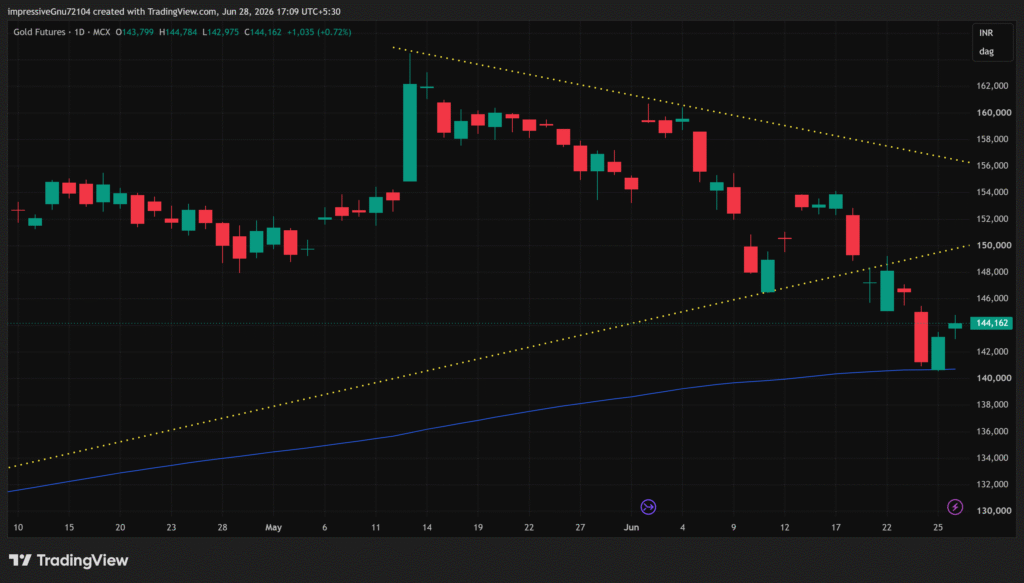

Gold | MCX GOLD1!

The week confirmed the breakdown from the earlier compression structure. Price moved below the lower rising trendline and is now trading clearly beneath it, so the triangle setup should no longer be treated as intact. The compression pattern that had defined the structural bull case since the February lows has been broken.

The more important development, however, was the reaction at the 200-day EMA. The sharp selloff into the 1,41,000 to 1,42,000 zone was absorbed by demand, and price has bounced back toward 1,44,000. This bounce is still corrective rather than structural; gold has not reclaimed the broken lower trendline, and the 1,46,000 to 1,48,000 area is the first meaningful retest zone. Above that, 1,49,000 to 1,50,000 is the more significant breakdown retest area. But the fact that demand appeared at the 200-day EMA matters: this is the major long-term moving average that has historically separated cyclical corrections within bull markets from full trend reversals.

The market structure remains bearish for now: lower highs continue, the failure near 1,53,000 to 1,54,000 was decisive, and the lower trendline has been lost. But the 200-day EMA is still holding, which keeps the broader uptrend technically alive. A decisive close below the 200-day EMA would confirm a deeper structural weakening; a reclaim of 1,49,000 to 1,50,000 would suggest the breakdown is starting to fail.

| Key Takeaway: Gold has a confirmed breakdown below the lower rising trendline, but not yet a confirmed breakdown below the 200-day EMA. The short-term bias remains bearish below ₹1,46,000 to ₹1,50,000, but the 200-day EMA defence keeps the move from becoming a clean long-term breakdown. This is the level that separates a deep correction from a full trend reversal. For Indian market participants, the rupee added negligibly to the decline in the week ending June 26; MCX gold tracked COMEX closely. The duty-and-rupee cushion did not help, but it did not amplify either. |

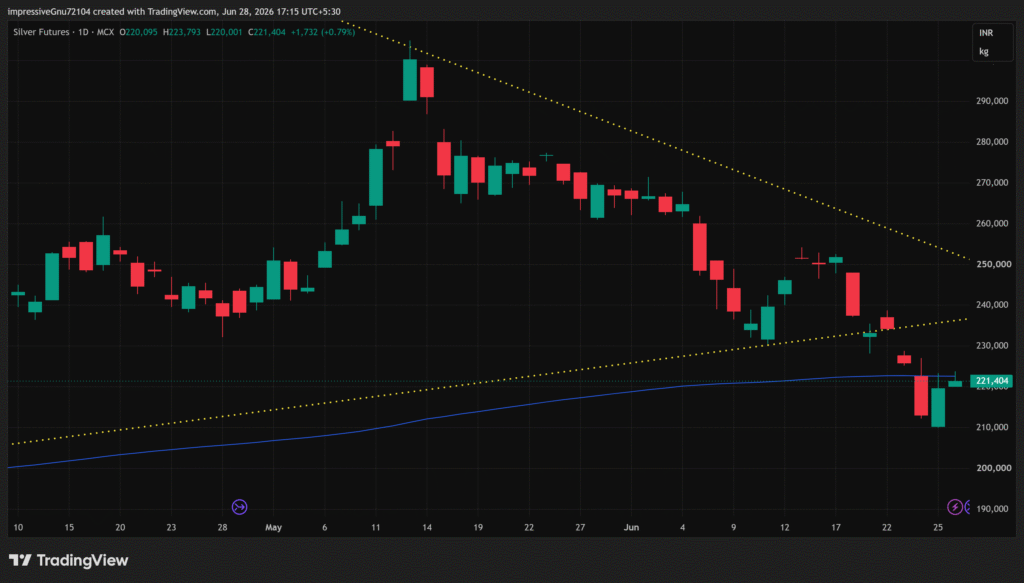

Silver | MCX SILVER1!

Silver remains structurally weaker than gold. Price has broken below the lower rising trendline and is now trading around or marginally below the 200-day EMA, rather than clearly defending it. The latest candles show a relief bounce from the 2,10,000 to 2,15,000 demand area, with price recovering to close near 2,21,000, but this recovery has only brought price back to the 200-day line, not above it with conviction.

The 2,25,000 to 2,30,000 area is now the first major supply zone. If silver fails there, the 200-day EMA region effectively turns from support into resistance, which would be a more decisive structural break than gold has shown. The prior failed recovery near 2,48,000 to 2,52,000 remains important: price could not reclaim that zone, rolled over, broke 2,35,000 to 2,38,000, and then expanded lower through both the lower trendline and the 200-day EMA area.

The compression pattern is now broken, and the bearish structural shift is confirmed on the daily chart. Silver is in a post-breakdown relief bounce, and the structure remains bearish unless price reclaims 2,25,000 to 2,30,000 first, then 2,35,000 to 2,38,000. The gold-silver ratio widening toward 70:1 is the cleanest expression of silver’s underperformance: silver has cheapened significantly relative to gold since the early May highs, but the broader rate-and-dollar environment has not yet produced the trigger for that cheapening to reverse.

| Key Takeaway: Silver has a confirmed breakdown below the lower rising trendline and is struggling around the 200-day EMA. The current bounce is reactive, not yet a reversal. The chart remains bearish below ₹2,25,000 to ₹2,30,000 and ₹2,35,000 to ₹2,38,000. The contrast with gold is meaningful: gold reacted from the 200-day EMA, while silver has pushed through it. The gold-silver ratio at approximately 70:1 reflects how much silver has cheapened relative to gold in this correction. Whether that represents an opportunity or a warning depends entirely on whether the industrial deficit story can reassert itself against the rate-cycle and dollar headwinds. |

Watch in the Days Ahead:

- Weekend escalation between US and Iran: After the article’s reporting period closed, the situation deteriorated significantly. US forces struck Iranian military targets on June 26 and again on June 27 in response to the Ever Lovely attack. Iran retaliated with missile and drone attacks on US-linked sites in Bahrain and Kuwait in the early hours of June 28 and struck a Panamanian-flagged tanker (M/T Kiku) carrying more than two million barrels of crude. President Trump warned that the United States may be “forced to militarily complete the job” and stated that “the Islamic Republic of Iran will no longer exist” if attacks continue. The 60-day peace roadmap is now under its most serious stress test yet. A sustained re-escalation would reverse the recent oil decline, push inflation expectations back up, compress real yields, and provide a positive catalyst for gold and silver. The opposite holds if diplomacy stabilises.

- Rates path and the dollar: With at least one Fed rate hike (and potentially two) now expected in 2026, the dollar is likely to remain firm, which is structurally bearish for the metals. Any softening in upcoming inflation data, particularly if the weekend escalation does not lift oil meaningfully, would re-open the rate-cut conversation and ease the dollar headwind. Watch the 10-year TIPS yield (real yield, currently approximately 2.19%) more than the 10-year nominal yield (4.38%) for the cleanest signal on gold direction.

- Gold at the 200-day EMA: This is the structural line that separates a deep correction from a trend reversal. A reclaim of ₹1,49,000 to ₹1,50,000 would relieve immediate pressure and re-engage the broader uptrend. A clean close below ₹1,40,500 (the 200-day EMA itself) would confirm a structural break and open the path toward the prior April lows.

- Silver below the 200-day EMA: Silver has already pushed through its 200-day line and bounced back to it. Acceptance below ₹2,20,000 would confirm a structural breakdown. A reclaim of ₹2,25,000 to ₹2,30,000 would suggest the breakdown is failing and the metal is regaining footing.

- FOMC member commentary and July meeting setup: With Warsh having communicated the broad framework, the next several Fed speakers will fill in the gaps. New York Fed President John Williams stated this past week that inflationary pressures are expected to moderate but remain too high. Watch for any meaningful shift in tone from voting members ahead of the late-July FOMC.

- Q2 2026 gold demand data: Q1 2026 saw record central bank buying (244 tonnes) and bar-and-coin demand at 397.7 tonnes (the highest in years). Q2 data, due in late July, will indicate whether the structural physical bid has held through the rate-and-oil repricing or whether it has weakened.

Disclaimer: This article is for informational purposes only and does not constitute investment or trading advice. All prices are futures closing prices, MCX in INR, COMEX in USD. Past performance is not indicative of future results.

Authored by Dhawal Chotai